Introduction

The S&P 500 dropped roughly 9-10% from its January 2026 all-time high, hitting its lows in late March 2026.

Then it hit a new all-time high of 7,026 on April 15, just weeks later.

Now ask yourself honestly. Did you invest during the dip? Or did you wait to see what happened?

Most people waited. And by waiting, they missed the recovery entirely.

This is the problem with trying to time the market. Even professional fund managers cannot do it consistently. In fact, over 20 years, the average equity investor earned roughly 5.5% per year. The S&P 500 returned 9.9% per year over the same period. That 4.4% gap exists almost entirely because of bad timing decisions.

Dollar Cost Averaging (DCA) solves this problem completely.

Many investors look for short term trading advice in USA stocks to navigate volatile markets. But for long-term wealth building, DCA is one of the most reliable strategies available. This guide explains exactly what DCA is, how it works, and why it belongs in every investor's toolkit.

This guide explains exactly what DCA is, how it works, and why it is one of the most powerful strategies for long-term investing, especially during volatile markets like we have right now.

What Is Dollar Cost Averaging?

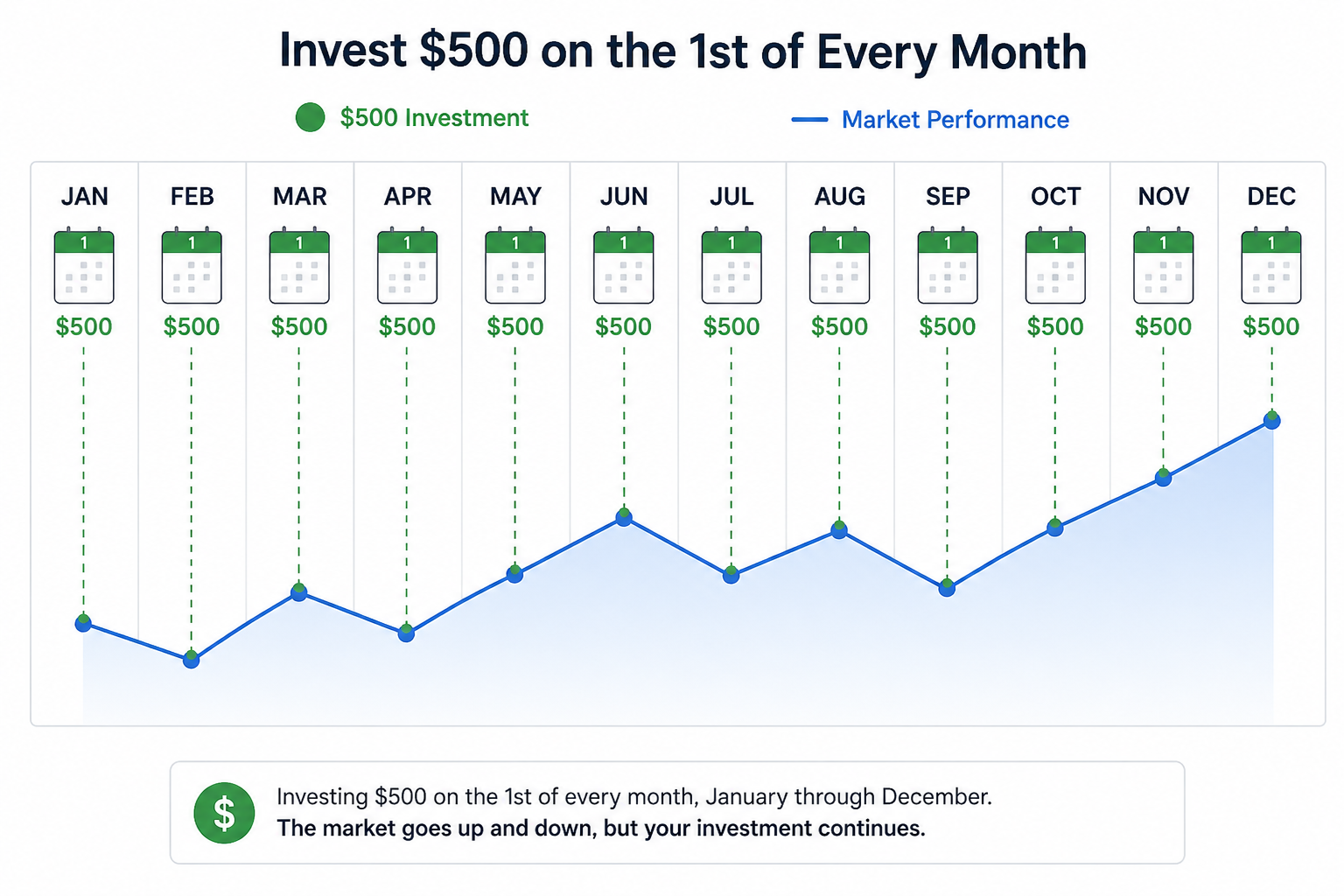

Dollar Cost Averaging means investing a fixed amount of money at regular intervals.

Same amount. Same schedule. Every time. Regardless of whether the market is up or down.

You are not trying to pick the perfect moment to invest. You are simply investing consistently and letting time do the work.

Charles Schwab, one of America's largest brokers, describes DCA simply as "investing a fixed dollar amount on a regular basis, regardless of the share price."

That is it. Nothing complicated about it.

How Does DCA Work?

Here is a simple three month example.

You invest $500 every month into an S&P 500 ETF.

Month Share Price Shares Bought Month 1 $50, 10 shares Month 2 $40, 12.5 shares Month 3 $55 9.1 shares

Total invested: $1,500. Total shares owned: 31.6 shares. Average cost per share: $47.47.

Notice something important. The average market price across those three months was $48.33. But your average cost was $47.47. You paid less than the average price automatically.

This happens because when prices dropped in Month 2, your $500 bought more shares. You got more for the same money without doing anything.

This is the core power of DCA. Price drops work in your favour instead of against you.

Does DCA Actually Work?

Here is real data from a verified backtest by Tradealgo, using actual S&P 500 price history.

An investor who put $500 every month into SPY (the S&P 500 ETF) starting January 2020 lived through all of this:

- A 34% pandemic crash in March 2020

- A 2022 bear market where the S&P 500 fell 25% peak-to-trough

- Multiple geopolitical shocks

The result? A 50%+ return over 5 years. Despite investing through one of the most turbulent periods in modern stock market history.

The DCA investor who kept buying through the 2020 crash bought shares at the March lows. When the market recovered, those cheap shares produced the biggest gains.

The investor who panicked and stopped investing missed those gains entirely.

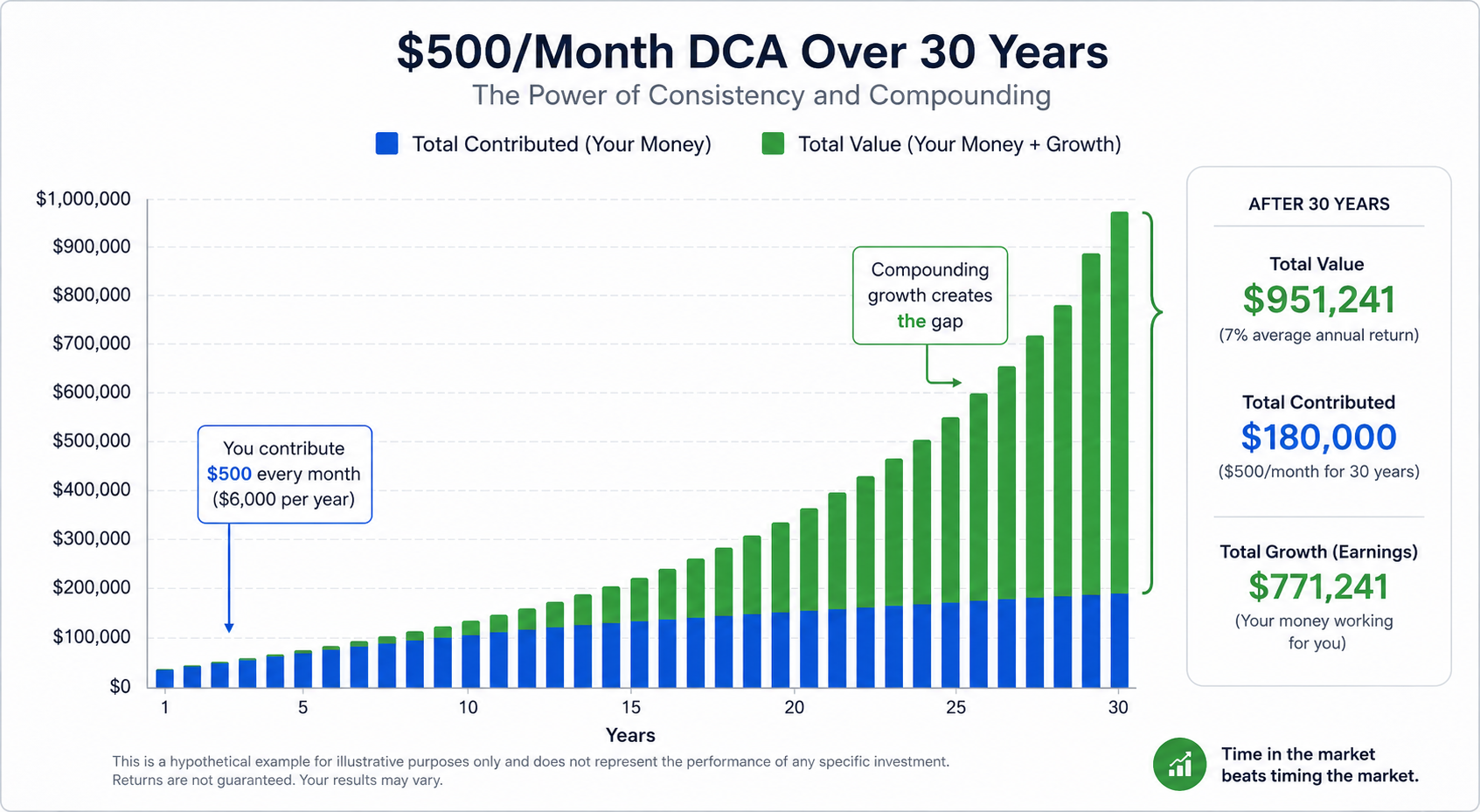

And over a longer horizon? According to Tradealgo's analysis, $500 per month invested at a 10% annual return grows to over $1.1 million in 30 years.

Is DCA Better Than Lump Sum Investing?

This is one of the most searched questions about DCA. The honest answer is nuanced.

Historically, lump sum investing beats DCA about 66% of the time. This is because markets generally rise over the long term. If you invest everything at once and the market goes up from there, you earn more.

But here is the catch.

If you invest a lump sum just before a crash like someone who put everything in at the S&P 500's peak in January 2026 before the Iran war drawdown the short-term loss can cause panic selling.

DCA removes that risk entirely. Your next scheduled investment actually benefits from the price drop, buying more shares at the lower price.

The real winner of DCA is not the maths. It is your behaviour. DCA keeps you invested through crashes. And staying invested is what builds wealth.

How Much Should I Invest With DCA?

A common starting point recommended by financial educators is 10% to 20% of your monthly income.

But the amount is less important than the consistency.

$100 per month invested consistently beats $5,000 invested once and never again.

Most US brokers including Fidelity, Schwab, and Interactive Brokers let you automate DCA. You set the amount, the date, and the asset. The investment happens automatically every month without you needing to think about it.

That automation is part of what makes DCA so powerful. You remove human emotion from the equation entirely.

Should I Stop DCA During a Market Crash?

No. And this is probably the most important thing in this entire blog.

Stopping DCA during a crash is the single worst thing you can do.

Here is why. When markets drop, your fixed monthly investment buys more shares at lower prices. Those are exactly the shares that generate the biggest returns when the market recovers.

The investors who stopped DCA in March 2020 during the pandemic crash missed the single fastest recovery in stock market history. The S&P 500 recovered all its losses within approximately five months of the March trough, hitting a new all-time high on August 18, 2020.

The DCA investor who kept going through that crash came out significantly ahead.

Warren Buffett put it simply. Be greedy when others are fearful. DCA automates this principle without requiring any courage or decision-making from you.

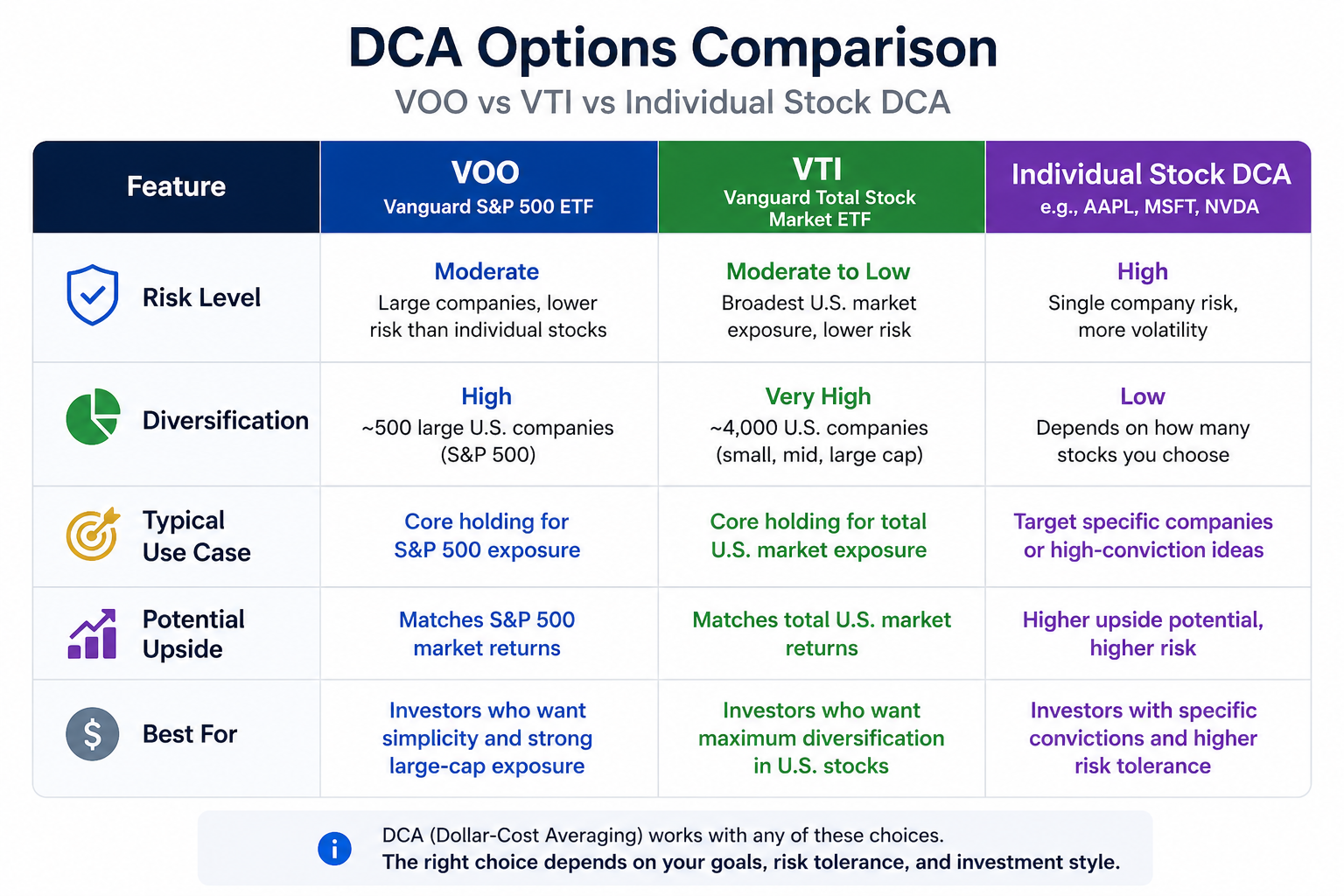

What Are the Best Assets for DCA?

DCA works best on diversified assets with long-term growth trends. The most common choices for US investors are:

S&P 500 index funds: VOO or SPY. You own 500 of America's largest companies in one position. This is the most widely recommended DCA vehicle.

Total market ETFs: VTI covers the entire US stock market, including small and mid-cap companies.

Individual quality stocks: DCA into strong individual stocks like Apple or Microsoft can work, but it concentrates your risk. If the company underperforms permanently, you have compounded a bad position. Use with caution.

DCA into highly speculative or volatile single stocks is risky. The strategy works best when the underlying asset has a strong long-term upward trend.

The Bottom Line

Dollar Cost Averaging is simple, but incredibly effective.

Instead of trying to predict market highs and lows, DCA helps you build wealth by investing consistently through every market condition.

Here is what matters most:

- Invest a fixed amount on a regular schedule

- Market drops help you buy more shares at lower prices

- Staying invested during crashes is where the biggest long-term gains often come from

- Diversified index funds like Vanguard S&P 500 ETF or Vanguard Total Stock Market ETF are among the most popular DCA choices

- Over time, consistency and compounding matter far more than perfect timing

Markets will always have uncertainty whether it is inflation, interest rates, wars, or recession fears. DCA removes the need to constantly predict what happens next.

DCA builds long-term wealth steadily over time. But some investors also combine it with swing trading in the US stock market to take advantage of shorter-term market opportunities while keeping a disciplined long-term investment strategy in place.

You invest consistently. You stay patient. And you let time and compounding do the heavy lifting.