Introduction

Most people know they should start investing early. They have heard it a hundred times. But hearing it and actually seeing what it means in real dollars are two very different things.

The gap between starting at 25 and starting at 35 is not just ten years of extra investing. It is often the difference between retiring comfortably and working longer than you ever planned. The numbers, when you lay them out clearly, are quietly shocking.

Let us look at what actually happens. With real math, not vague advice.

The one rule that makes early investing so powerful

Before the numbers, one simple idea needs to be clear. Compounding.

Here is the simplest way to think about it. You invest some money. It earns a return. Next year, that return also earns a return. Then that return earns a return. On and on, for decades.

In the early years, it barely feels like anything is happening. But somewhere around the fifteen or twenty year mark, the curve bends sharply upward. Money starts growing faster than you are putting it in. At that point, time itself is doing most of the heavy lifting.

Einstein reportedly called compound interest the eighth wonder of the world. Whether he actually said that or not, the math behind it is genuinely remarkable.

The S&P 500, America's most trusted broad market index, has returned an average of roughly 10 percent per year over the last 30 years. That is the number we will use. It is the verified long-term average from Fidelity, Trade That Swing, and multiple financial research sources as of May 2026.

While many investors actively follow US stock market recommendations for trading and investment opportunities, this article focuses on a different factor that often has an even bigger impact on long-term wealth creation: the age at which you begin investing.

Now let us see what that 10 percent actually does to three different investors.

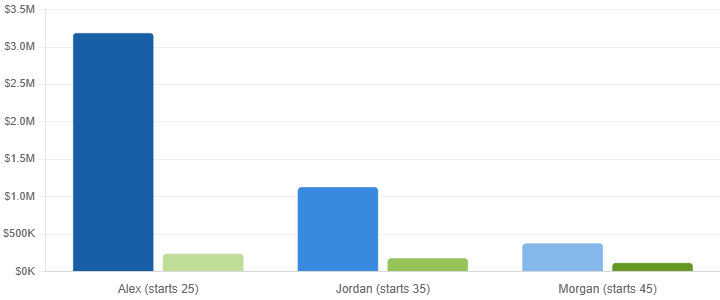

Meet Alex, Jordan, and Morgan

Three people. Same goal. Retire at 65 with as much money as possible. Same monthly investment of $500. Same 10 percent average annual return from a simple S&P 500 index fund. The only difference is when they start.

Alex starts at 25. Jordan starts at 35. Morgan starts at 45.

Here is what each of them ends up with.

Alex ends up with $3.19 million. Jordan ends up with $1.13 million. Morgan ends up with $379,000.

Same $500 every month. Same investments. Same market. The only variable was age.

Alex put in $240,000 of their own money over 40 years. The market turned it into $3.19 million. That is roughly $2.95 million in pure growth from compounding.

Jordan put in $180,000. Ended up with $1.13 million. Respectable. But less than a third of what Alex has, despite investing only $60,000 less.

Morgan put in $120,000. Ended up with $379,000. Still better than nothing. But nowhere close.

Ten extra years gave Alex three times Jordan's final number. Twenty extra years gave Alex more than eight times Morgan's final number. That is not a small difference. That is a completely different retirement life.

The decade that does the most damage

Here is the part of this story most people find hardest to believe.

The ten years Alex invested between age 25 and 35, before Jordan had even started, are worth more than all of Jordan's 30 years of investing combined.

In other words, those first ten quiet years, when Alex was young and the amounts were small and nothing felt impressive, turned out to be the most valuable decade of their entire investing life.

This is what compounding does at the far end. The money invested earliest has the longest time to multiply. A dollar invested at 25 has 40 years to grow. A dollar invested at 35 has only 30. That ten-year gap, compounding at 10 percent, makes the first dollar worth roughly 2.6 times more than the second.

What if Jordan tries to catch up?

A fair question. Jordan missed a decade. Can they make up the difference by investing more?

The answer is yes, technically. But the amount required to close the gap is sobering.

To match Alex's $3.19 million by retirement, Jordan would need to invest around $1,400 per month instead of $500. That is nearly three times as much, every single month, for 30 years straight.

Most people cannot simply triple their monthly investment on demand. Which is exactly the point. Time is the one resource that cannot be bought back at any price.

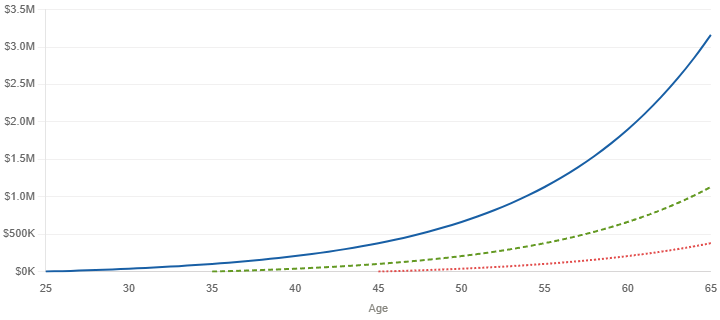

How the gap grows year by year

The chart below shows something even more striking. It is not just the final number that differs. The gap between the three investors widens every single year. The longer the wait, the harder it becomes to catch up.

Notice how the curves stay relatively close in the early years. Then around the 45 to 55 age range, Alex's line bends sharply upward. That bend is compounding entering its most powerful phase. And it is a phase that only happens when you have been in the market long enough.

Jordan's line follows a similar shape but starts a decade later. Morgan's barely has time to bend before retirement arrives.

The most common excuses, and what they actually cost

Most people who delay do not do it on purpose. They have reasons. Good ones, usually.

"I will start once my student loans are paid off." "I need to save for a house first." "I will invest more seriously after my next raise."

These feel responsible. And often they are. But the invisible cost of each delay is real, and it compounds just like a portfolio does.

Waiting just five years, say starting at 30 instead of 25, cuts Alex's final number from $3.19 million down to roughly $1.97 million. That five-year delay costs over a million dollars in retirement wealth.

Waiting ten years costs two million dollars.

Not because of lost contributions. Because of lost time for compounding to work.

So what should someone who is already 35 or 45 actually do?

The honest answer is simple. Start now. Not next year. Not after the next bonus.

The second best time to plant a tree is today. That saying exists for a reason.

If you are 35, you still have 30 years. Jordan's $1.13 million is a genuinely solid retirement foundation. Not three million, but not nothing either. And if you can invest more than $500 a month, the gap narrows significantly.

If you are 45, the math is tighter. But 20 years of consistent investing at a decent rate still builds real wealth. The key is to increase the monthly contribution where possible and avoid the temptation of chasing risky investments to make up for lost time quickly. That almost always makes things worse.

The worst thing anyone at 35 or 45 can do is look at Alex's number, feel discouraged, and do nothing.

Whether you are just starting out or already building a portfolio, one lesson consistently appears in quality USA stocks advisory research: time in the market is usually far more valuable than trying to predict the next market move.

Also read: Timing the Market vs Time in the Market: What US Data Say About Market Timing Myths

A simple closing thought

The most expensive financial mistake most Americans make is not a bad stock pick. It is not paying too much in fees. It is not even missing a great opportunity.

It is waiting.

Every year of delay is not just one year of lost investing. It is one less year for every previous dollar to compound. The cost is invisible while it is happening. It only becomes visible decades later, when the numbers land.

Alex did not become a millionaire because of genius stock picks or market timing. Alex became a millionaire because of something far simpler and far more available. An early start and the patience to leave it alone.

That is a decision anyone can make. The only question is when.