Introduction

Every three months, millions of investors do the same thing. They check what Warren Buffett bought. They check what he sold. Then they copy it.

The thinking makes total sense. The most successful investor alive is showing you his exact bets. Why would you look away?

But almost nobody asks the most important question. If you had actually copied him, what money would you have made?

We dug into the real numbers. The answer will surprise you.

What you think you are copying, and what you are actually copying

Here is something most people never realise. Berkshire Hathaway is not just a list of stocks.

Think of it like an iceberg. The stocks you can see are just the tip. Below the surface, Berkshire owns entire companies outright. GEICO, one of America's biggest car insurance companies. BNSF Railway, which moves goods across the United States. Berkshire Hathaway Energy, which powers millions of homes. Dozens of other businesses that quietly earn money every single day.

On top of that, Berkshire is sitting on nearly $400 billion in cash. That is not a typo. Four hundred billion dollars, parked and ready.

The 60-year track record everyone talks about comes from all of this together. The companies. The cash. The insurance float. The private deals that never appear anywhere public.

When you copy the 13F filing, which is the public document showing Berkshire's stock positions, you are only copying the visible tip. The rest of the iceberg stays with Berkshire.

What the latest filing actually shows

On May 15, 2026, Berkshire filed its latest 13F with US regulators. This one was different from all the others.

Warren Buffett, now 95, retired as CEO at the end of 2025. He remains Chairman of the Board and still makes some investments. But Greg Abel is now the new CEO, and he took charge on January 1, 2026. This was his first quarterly filing.

And Abel came out swinging.

In just one quarter, Berkshire sold out of Visa, Mastercard, Amazon, UnitedHealth, and more than a dozen other companies. At the same time, it more than tripled its investment in Alphabet, which is Google's parent company. It also made a fresh $2.6 billion bet on Delta Air Lines.

The total portfolio shrank from around $274 billion to $263 billion. The number of stocks fell from 42 all the way down to 29.

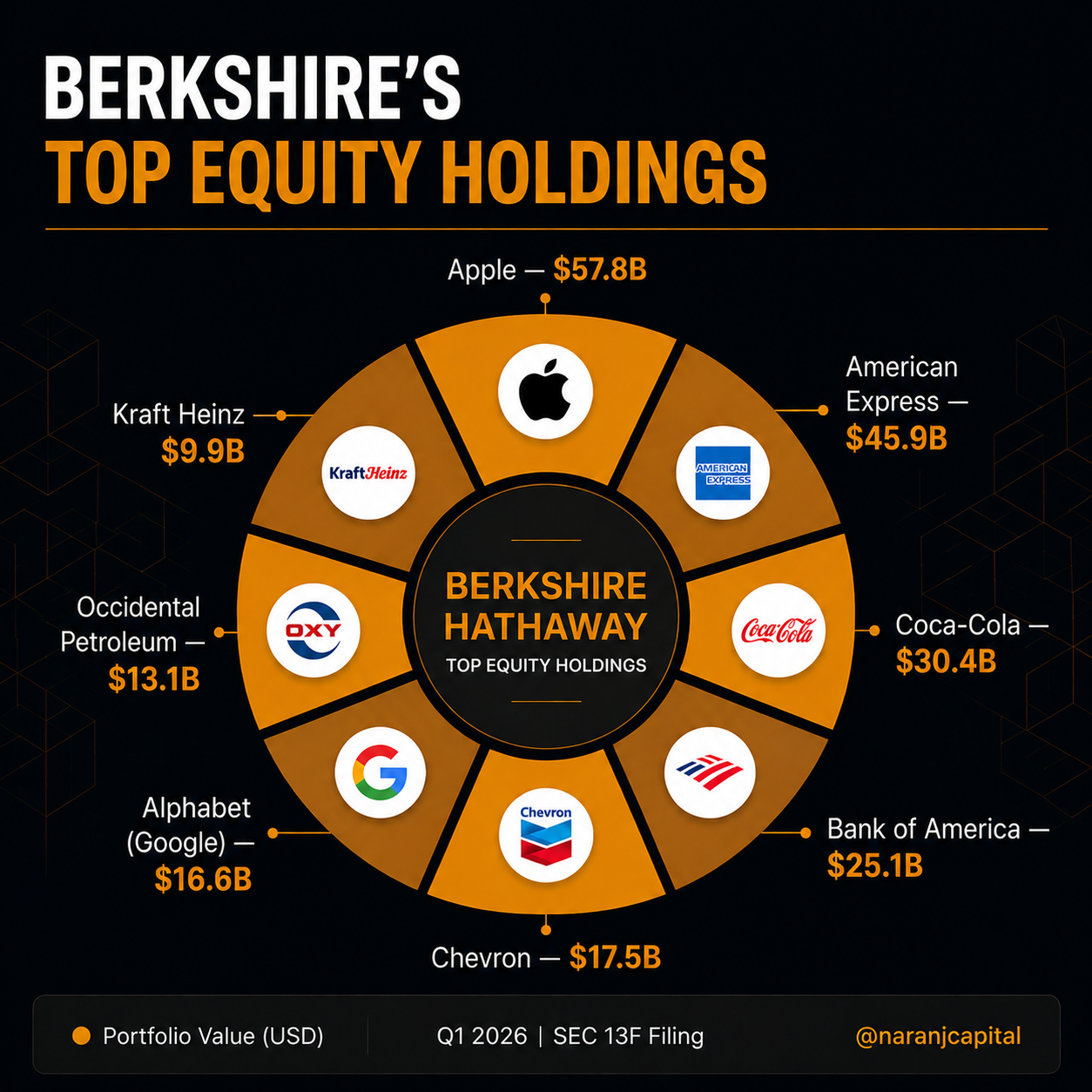

Today, just five companies make up around 68 percent of the entire portfolio. Apple, American Express, Coca-Cola, Bank of America, and Chevron. Apple alone is about 22 percent of everything.

So if you copy this portfolio today, you are basically putting two thirds of your money into five big, well-known, slow-moving companies. That is not necessarily wrong. But it is worth knowing before you act.

The 60-year number that dazzles everyone

Here is the headline figure that makes every investor want to follow Buffett. From 1965 to 2024, Berkshire grew at 19.9 percent per year on average. The S&P 500, which is the index of America's biggest companies, grew at only 10.4 percent per year.

That gap sounds small. But compounding over decades makes it enormous.

A hundred dollars put into Berkshire in 1965 would be worth around five and a half million dollars today. The same hundred dollars in a simple index fund would be worth around forty thousand dollars. Same starting point. Wildly different ending.

But here is what the big number hides. That extraordinary performance was mostly built decades ago, when Berkshire was small and nimble. It could jump in and out of positions quickly. It could double its money on relatively small bets.

Today, Berkshire is one of the largest companies on the planet. You cannot move hundreds of billions of dollars the same way you move a few million. The machine became too big for its old tricks.

The 45-day problem nobody talks about

This is the part that really kills the copycat strategy.

Berkshire is allowed to wait 45 days after each quarter ends before publishing its positions. So the filing you read in May shows positions that were built between January and March. By the time you see what Buffett or Abel bought, those trades are already months old.

And here is the problem. The moment the filing goes public, everyone rushes to buy the same stocks. The price jumps immediately. You end up buying after the move has already happened.

A research study from 2008 tested exactly this. It found that following Berkshire's filings with a one month delay would have beaten the S&P 500 by around 10.75 percent per year from 1976 to 2006.

Impressive, right? But that period was when Berkshire was much smaller. Positions were built quickly. The delay gap mattered less. After 2006, as the portfolio grew into hundreds of billions, that advantage slowly disappeared. The last decade performance confirms it.

The one edge you are giving away for free

Here is the strange irony of copying Berkshire.

You as an individual investor actually have something Berkshire does not. Speed. You can buy a stock in seconds. You can sell it in seconds. You do not move the market. Nobody even notices.

Berkshire cannot do that. When it wants to build a position worth several billion dollars, it takes months of carefully buying small amounts so it does not push the price up against itself.

The moment you try to mirror a $263 billion portfolio, you throw away your biggest advantage. You take on all the limitations of a giant institution without getting any of the benefits that make being that giant institution worthwhile.

So what return would you actually get?

Here is the straight answer. If you had copied Berkshire's publicly listed stock positions over the last 20 years, rebalancing every quarter 45 days after each filing, you would have made roughly the same as the S&P 500.

Some years better. Some years worse. On average, market returns.

You could have saved yourself all that work by simply putting your money into a low-cost index fund.

Copy the thinking, not the list

Mohnish Pabrai, one of the most well-known followers of Buffett's approach, has a name for what most people do wrong. He calls it half-baked cloning. You see the stock. You copy the stock. But you have no idea why Buffett bought it, how long he planned to hold it, or how much pain he was willing to sit through before selling.

So when it drops 30 percent, you panic and sell. Buffett was planning to hold for fifteen years.

There is also something new to consider. This was Greg Abel's first quarter running the show. Nobody fully knows yet how his style differs from Buffett's. What sectors he likes. What valuations he is comfortable with. You would be copying a portfolio whose captain just changed, based on his very first 90 days of decisions.

Investors who treat every 13F as ready-made swing trading picks for US stocks are misreading what the document actually is. It is a backward-looking record of a long-term owner's positions. It was never meant to tell you what to buy tomorrow morning.

The real things worth copying are not on any list. Buy businesses that customers keep coming back to. Do not overpay. Hold when things get scary. Keep some cash for when markets fall. Never speculate on things you do not understand.

Those simple habits built the 19.9 percent annual return over 60 years. No single stock did that. No filing did that. A way of thinking did that.

The simple truth

The filing is real. The 45-day lag is real. The recent decade of underperformance is real. The new CEO is real.

Copying the stock list is not a shortcut to Buffett's returns. The shortcut was always copying his principles.

Most investors spend years chasing the list. The smart ones spend those same years learning the US stock market signals that actually matter, which are patience, discipline, and the willingness to hold while everyone else panics.

That gap between copying the trades and copying the thinking is where most investors quietly leave their money behind.