- Naranj Research Desk

- 🇸🇦 Saudi Stock Market

- 🇺🇸 USA Stock Market

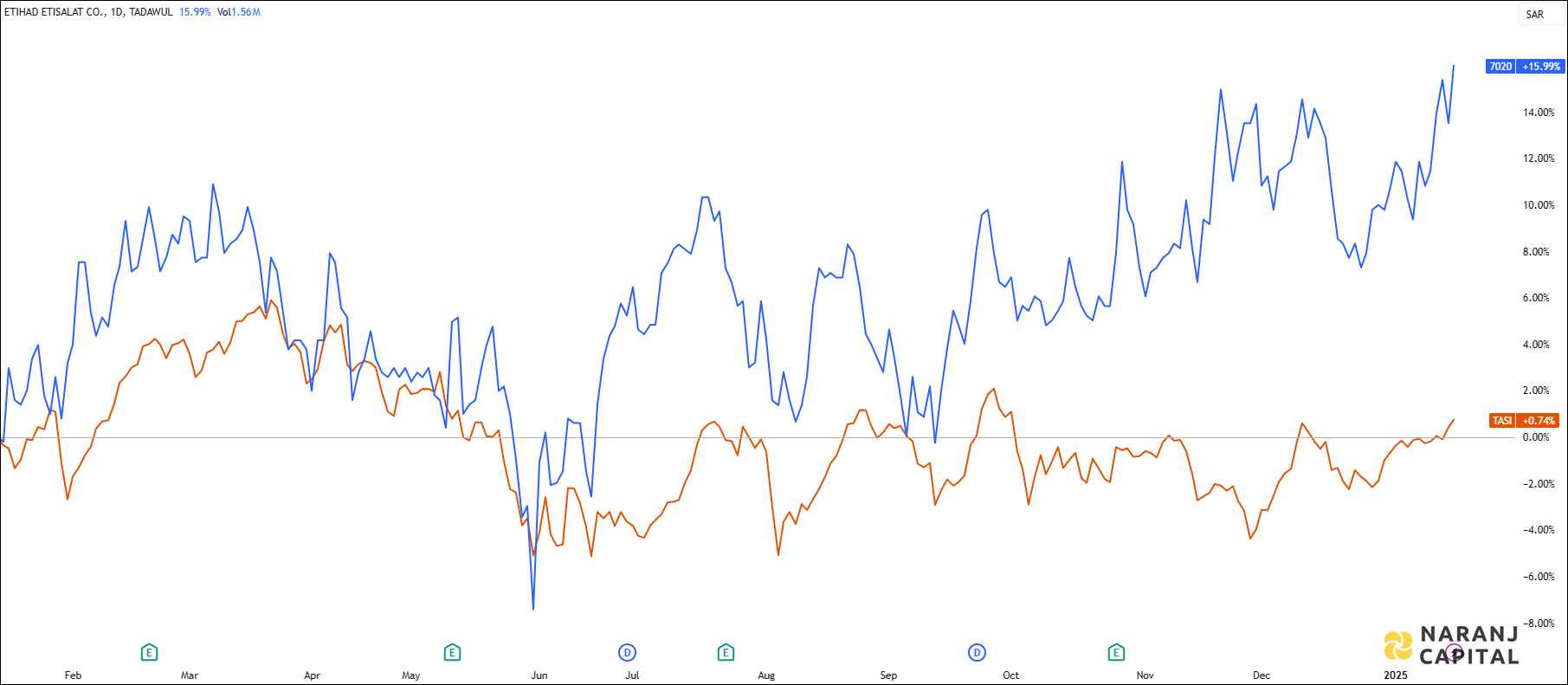

The chart highlights Etihad Etisalat's strong performance, with a 15% annual return that outshines the Tadawul all-share index.

Saudi Arabia's telecommunications sector is poised for significant growth in the coming years, driven by the government's Vision 2030 initiative. This ambitious plan includes substantial investments in telecommunications infrastructure, particularly in building a national fiber optic network and expanding 5G services.

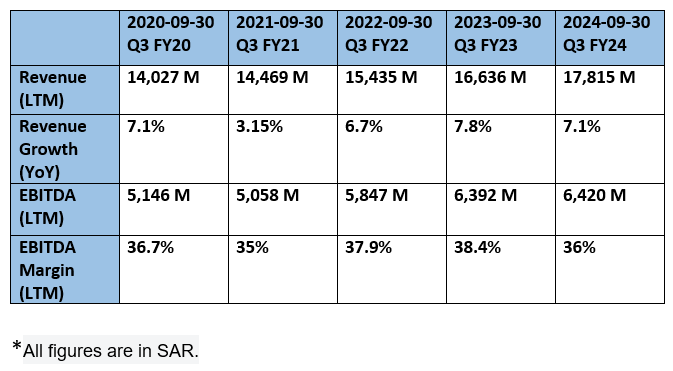

As a leading telecommunications provider, Etihad Etisalat (Mobily) is strategically positioned to capitalize on this momentum., supported by its strong financial performance and positive technical aspects.