Introduction

Imagine it's 1970.

Doctors are telling people to quit smoking. Warning labels are going on cigarette packs. Governments are running anti-smoking campaigns. The whole world seems to agree: the tobacco industry is finished.

A sensible investor looks at tobacco stocks and says: "This is a dying business. I'm staying away."

That sensible investor made a terrible mistake.

Between 1968 and 2015, Philip Morris, the company that makes Marlboro cigarettes, grew an investor's money by roughly 4,000 times. The S&P 500, which tracks America's top 500 companies, grew money by about 70 times in the same period.

Philip Morris won by a mile. Despite selling a product that fewer and fewer people were buying.

How?

The Thing Most People Get Wrong

Here's how most people think about it:

"Fewer people are smoking every year. So the business must be making less money. Less money means a bad investment."

Makes sense, right?

But there's a problem with that thinking.

Making less money and selling less of a product are two different things.

Tobacco companies figured out a simple trick. If you can't sell more cigarettes, just charge more for each one.

And that's exactly what they did.

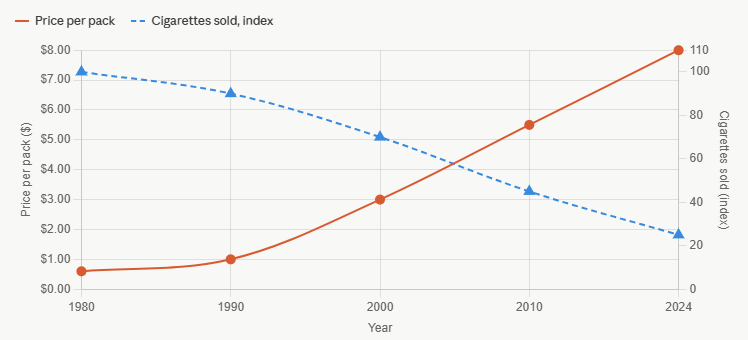

In 1980, a pack of cigarettes in the US cost about 60 cents. By 2024, the same pack cost over $8. That's a price rise of more than 1,200%.

Meanwhile, yes, the number of cigarettes sold dropped by about 75%.

But do the quick math. You're selling one-fourth the cigarettes and charging 13 times more. The company is still making a lot of money.

Why Smokers Just Keep Paying

So why don't smokers just say "enough" and quit when prices go up?

Because nicotine is addictive.

That one fact is the entire secret of the tobacco business.

Think about it this way. If your local tea stall raises the price of tea by 50%, you might switch to coffee, or skip tea some mornings. You have options.

But if someone is addicted to cigarettes and the price goes up, they don't really have that choice. They need the cigarette. So they pay.

This is what experts call pricing power. The ability to charge more without losing customers.

For investors seeking positional trading advisory in USA stocks, pricing power is often one of the most important characteristics to look for. Companies that can consistently raise prices without significantly hurting demand often generate stronger long-term shareholder returns.

Very few businesses in the world have this kind of power. Tobacco companies have had it for over a century.

A Business That Practically Runs Itself

Here's another thing that makes tobacco companies special: they don't need to spend much money to stay in business.

Think about what other companies have to deal with:

A tech company has to hire expensive engineers every year just to keep up. A car company has to spend billions building new models. A phone company has to constantly upgrade its network.

A cigarette company? The recipe for a cigarette hasn't changed in decades. Once the factory is up and running, it just keeps running. There's no need to constantly reinvent anything.

This means every year, after paying all their costs, tobacco companies are left with a huge pile of extra cash. More cash than they actually need to run the business.

What do they do with all that cash? They give it to their investors.

Getting Paid While You Wait

Tobacco companies pay something called a dividend. Think of it as a thank-you payment the company sends to its investors, usually every three months.

Philip Morris and its spinoff company Altria have raised this payment every single year for decades. That's not common. Most companies cut dividends during tough times. These companies kept raising them.

Now here's where it gets really powerful.

Imagine you receive a dividend payment. Instead of spending it, you use that money to buy more shares. Next time, you earn a dividend on those extra shares too. Then you buy even more shares with that.

Over 30 or 40 years, this snowballs into a huge amount. You're essentially earning money on your money, again and again.

A finance professor named Jeremy Siegel studied this closely. He found that a huge chunk of Philip Morris's incredible returns came not just from the rising stock price, but from these dividends being reinvested year after year.

The dividend was doing a lot of the heavy lifting.

The "Too Controversial to Touch" Effect

Here's a twist that most people don't expect.

Because tobacco is harmful, many large investors simply refuse to buy tobacco stocks. Pension funds, university investment funds, and funds that focus on ethical investing all have rules that say: no tobacco.

That removes a huge amount of money from ever buying these stocks.

When fewer people are willing to buy a stock, the price stays low. A low price compared to the company's earnings means the stock is cheap.

And cheap stocks, especially in businesses that keep generating cash, tend to give higher returns over time.

Think of it like buying a good house in a neighbourhood that has a bad reputation. The price is low because nobody wants to be there. But if the house keeps generating rental income, you end up doing very well.

Tobacco stocks have been in that "bad neighbourhood" for decades. Perpetually cheap. Perpetually ignored. And perpetually rewarding for patient investors.

The Shrinking Business That Still Made You Richer

This is the strangest part of the whole story.

Picture a pizza. The pizza represents all the profits a tobacco company earns each year.

As fewer people smoke, the pizza gets a little smaller each year. Bad news, right?

But here's the thing. As the business shrinks, a lot of investors sell their shares and leave. That means there are fewer people sharing the pizza.

So even though the pizza is smaller, each remaining person gets a bigger slice.

On top of that, tobacco companies use their extra cash to buy back their own shares from the market. That reduces the total number of shares even further. So each share you hold becomes worth more, automatically.

The result? The business is shrinking. But your investment is growing.

What's Happening Today?

Tobacco companies aren't just sitting still and waiting to die.

They're quietly shifting to new products. Philip Morris now sells IQOS, a device that heats tobacco instead of burning it. Altria sells nicotine pouches. British American Tobacco has a line of e-cigarettes.

The goal is the same as always: keep the customer hooked on nicotine, just through a newer delivery method.

Whether these new products will be as successful as cigarettes were is still unclear. But the cash that tobacco companies make from traditional cigarettes is funding all of this. That buys them time and options.

What Can We Learn From All This?

The tobacco story isn't about whether you should invest in cigarette companies. That's a personal decision.

It's about a much bigger idea.

One reason experienced investors and providers of US trading and investment advice study tobacco stocks is that they challenge conventional thinking. Strong investment returns do not always come from rapidly expanding industries; they often come from businesses with durable economics and disciplined capital allocation.

You don't need an exciting, growing industry to make great investments.

Sometimes the best investments are in boring, slow, even shrinking businesses, as long as those businesses:

Keep raising prices without losing too many customers. Don't need to spend a lot to stay in business. Return their extra cash to investors through dividends.

Tobacco companies did all three, for 50 years straight, while the whole world was rooting against them.

The market assumed tobacco was doomed and priced the stocks cheaply. But "doomed" businesses can still generate cash for a very long time. And if you buy them cheaply and collect their dividends patiently, the returns can be extraordinary.

The lesson: don't always follow the crowd when it comes to investing. Sometimes the business everyone is running away from is exactly where the money is.