- Naranj Research Desk

- 🇸🇦 Saudi Stock Market

- 🇺🇸 USA Stock Market

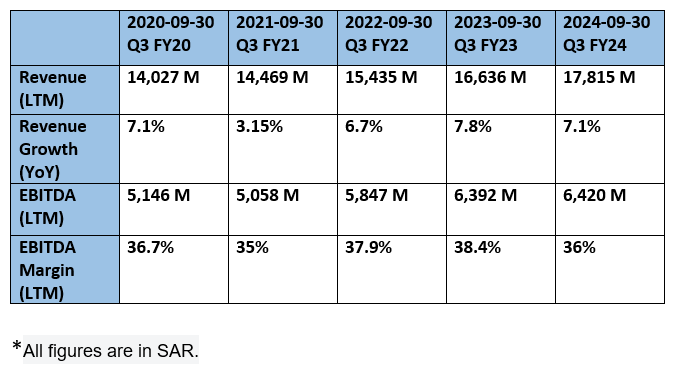

Etihad Etisalat Company, commonly known as Mobily, is a major telecommunications provider in the Kingdom of Saudi Arabia. Founded in 2004, Etihad Etisalat is headquartered in Riyadh, Kingdom of Saudi Arabia. The company builds and runs mobile phone networks and high-speed internet cables. They also sell mobile phones, set up phone systems, and fix telecommunication equipment.

They offer various other services such as information technology, application, billing, and testing support, as well as product marketing, process management, and financial services. The company also engages in telecommunication services, consulting, and office administration. Besides their main business, they invest in shares, bonds, and real estate. Mobily have a market capitalization of 42.2 Billion SAR [as of January 2025].

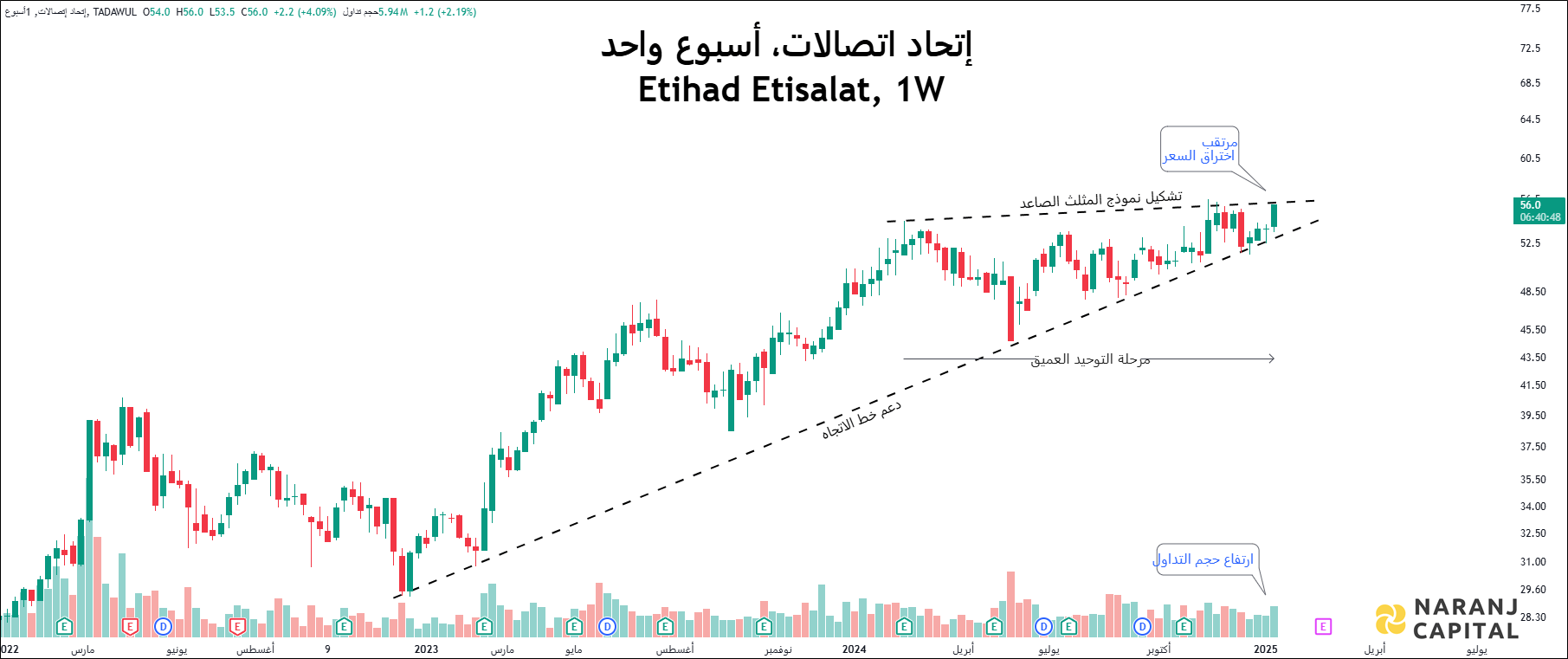

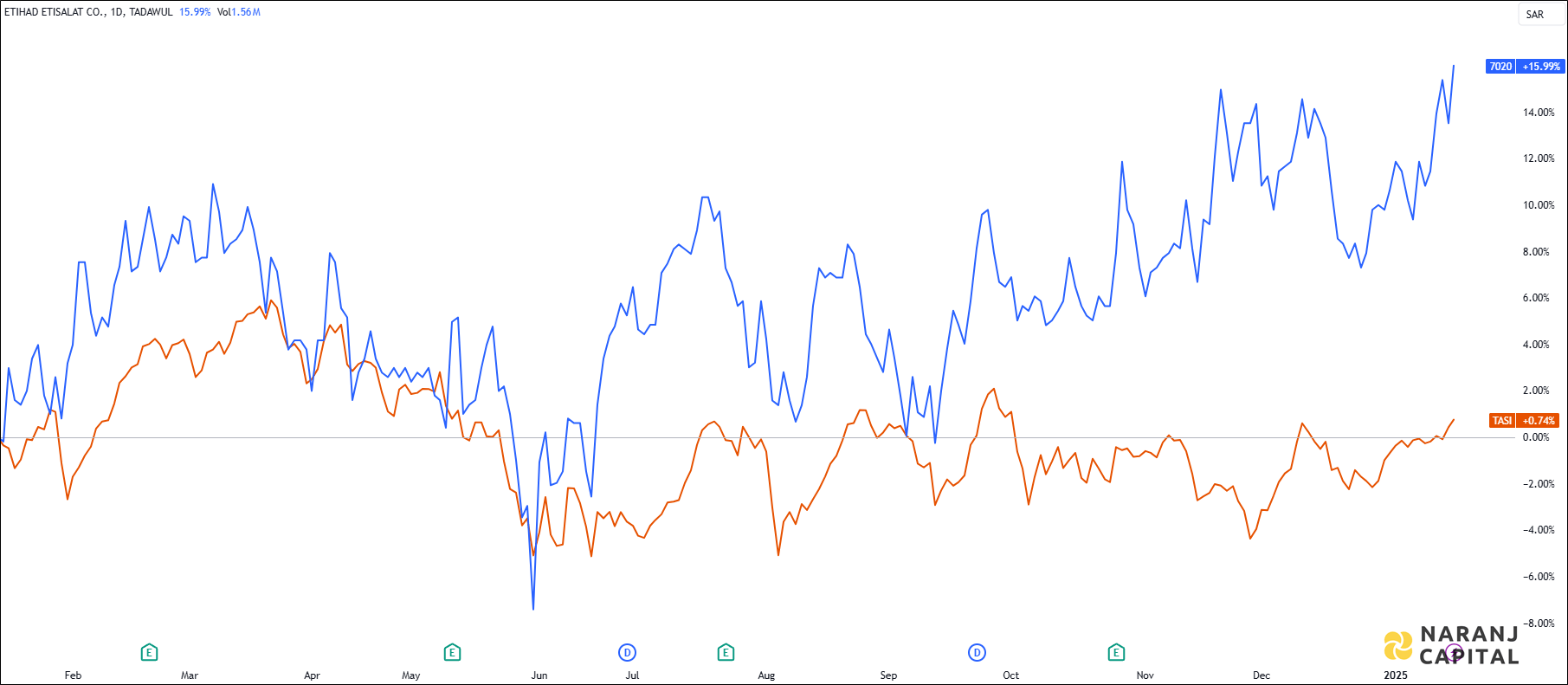

ETIHAD ETISALAT — TASI —

Saudi Arabia's telecommunications sector is poised for significant growth in the coming years, driven by the government's Vision 2030 initiative. This ambitious plan includes substantial investments in telecommunications infrastructure, particularly in building a national fiber optic network and expanding 5G services.

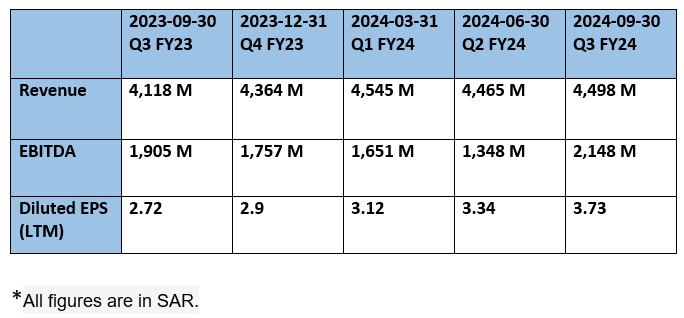

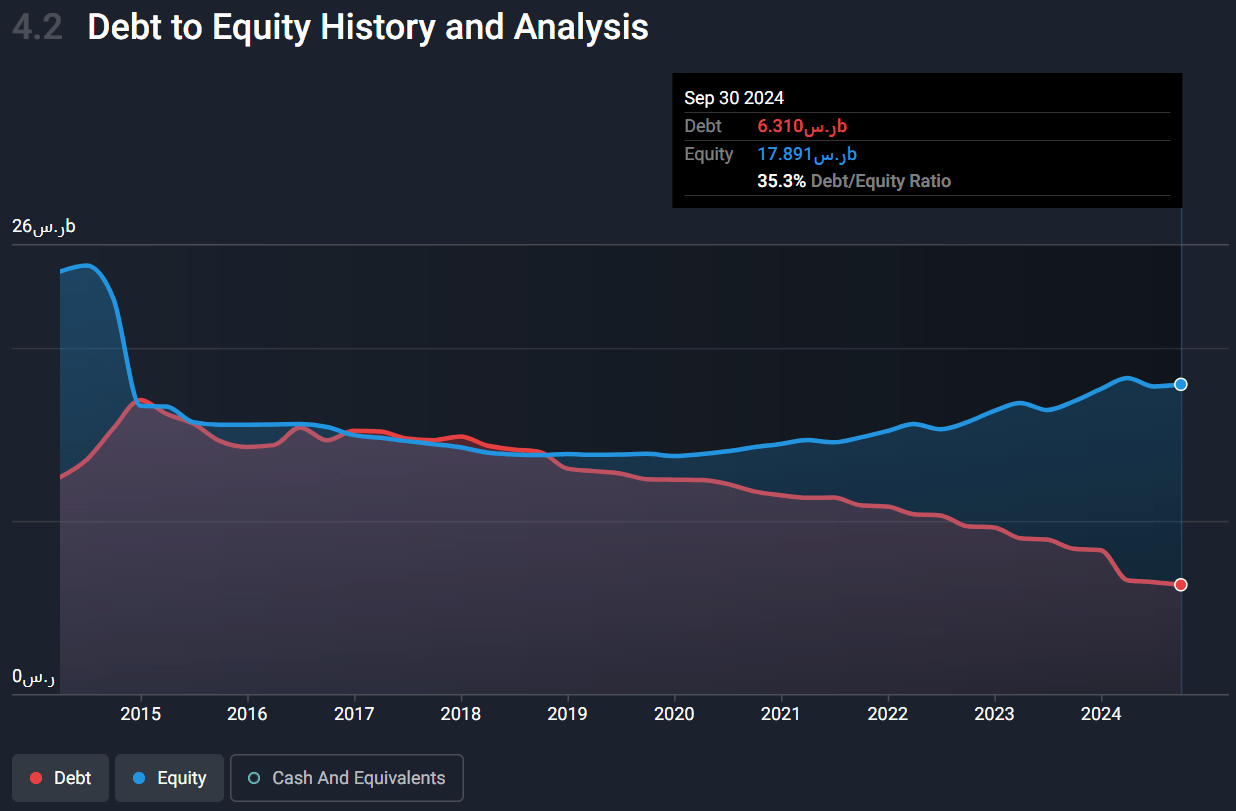

We give a “BUY” rating to Etihad Etisalat (Mobily). As a leading telecommunications provider, Mobily is strategically positioned to capitalize on this momentum, supported by its strong financial performance and positive technical aspects.

Looking to start your investment journey? Subscribe now to get exclusive access to our Premium Stock Trading Advice for Saudi Tadawul and take a step toward building long-term wealth.

Etihad Etisalat Company, commonly known as Mobily, is a major telecommunications provider in the Kingdom of Saudi Arabia. Founded in 2004, Etihad Etisalat is headquartered in Riyadh, Kingdom of Saudi Arabia. The company builds and runs mobile phone networks and high-speed internet cables. They also sell mobile phones, set up phone systems, and fix telecommunication equipment.

They offer various other services such as information technology, application, billing, and testing support, as well as product marketing, process management, and financial services. The company also engages in telecommunication services, consulting, and office administration. Besides their main business, they invest in shares, bonds, and real estate. Mobily have a market capitalization of 42.2 Billion SAR [as of January 2025].

ETIHAD ETISALAT — TASI —

Saudi Arabia's telecommunications sector is poised for significant growth in the coming years, driven by the government's Vision 2030 initiative. This ambitious plan includes substantial investments in telecommunications infrastructure, particularly in building a national fiber optic network and expanding 5G services.

We give a “BUY” rating to Etihad Etisalat (Mobily). As a leading telecommunications provider, Mobily is strategically positioned to capitalize on this momentum, supported by its strong financial performance and positive technical aspects.

Looking to start your investment journey? Subscribe now to get exclusive access to our Premium Stock Trading Advice for Saudi Tadawul and take a step toward building long-term wealth.